Asian Oil and Gas Industry Insight

The Asia-Pacific region is soon projected to lead the world in terms of economic growth. The region is also likely to continue to drive global energy demand in the years ahead. According to an offshore oil and gas research report conducted by Infield, the Asian market is forecasted to see a 54% increase in expenditure for offshore oil and gas infrastructure over the next five years, with South East Asia continuing to drive demand in the region.

Although, as consultants Wood Mackenzie estimate, Southeast Asia’s liquids production is declining and expected to drop from an estimated 879 million barrels of oil equivalent (boe) in 2013 to 838 million boe in 2018, gas production is set to grow at an annual rate of 2.5% from around 1.25 billion boe in 2013 to 1.45 billion boe by 2018.

Read More

Wood Mackenzie estimates that Southeast Asia holds about 60.92 billion boe in commercial and technical oil and gas reserves, while total yet-to-find (YTF) volume is estimated at 14.6 billion boe, of which liquids comprise 5.5 billion boe and gas 9.1 billion boe.

The bulk of the region’s recoverable reserves are located in Indonesia and Malaysia, which contribute 29.55 billion boe (48%) and 15.41 billion boe (25%), respectively.

Malaysia

China and Malaysia have been the key drivers of offshore capex in recent years, and Malaysia is forecast to continue to spend heavily in this regard. Twenty-four new discoveries were made in Malaysia in 2012 alone.

Malaysia has been using a combination of innovative contracts to promote development of marginal fields, enhanced oil recovery techniques to get more out of its large but aging fields, and floating liquefaction technology to monetize stranded gas fields. All this has resulted in boosting its hydrocarbon production which was in a state of decline only a few years back. To further buoy the sector in Malaysia, the Malaysian government has introduced favourable taxes and non-tax incentives for downstream businesses, which is anticipated to have a positive flow on effect to upstream activity.

Indonesia

Indonesia’s long-established oil and gas producing basins – Sumatra, Java and East Kalimantan are well explored, but the country still holds extensive oil and gas resources. According to Wood Mackenzie, Indonesia is estimated to hold about 3.67 billion boe of YTF reserves in the eastern basins, where large areas, both onshore and offshore, remain relatively unexplored.

Factors such as remoteness, large size, infrastructure deficiency and harshness of terrain make oil and gas exploration in this region challenging. Although deepwater exploration in the region is yet to see any encouraging results and ten international companies, having spent $1.65 billion over 2009-2012, failing to find commercially viable hydrocarbon reserves, the region still cannot be written off. There are areas which remain unexplored. What is needed is a more conducive regulatory climate, clarity on domestic market obligations (DMO) (DMO is the quantum of oil and gas production that the contractor has to allocate to the local market; generally set at 25%, but can go higher as well), appropriate incentives and adequate data points on the acreage to truly optimize Indonesia’s deepwater potential.

Vietnam

Vietnam has also increased exploration by moving into more challenging locations like the Song Hong Basin and the frontier Phu Khanh Basin. Italian Oil Company Eni and KrisEnergy are jointly developing two blocks in these new locations where they expect to unlock very large fields. Wood Mackenzie estimates that Vietnam holds about 4.78 billion boe of total remaining reserves, 62% in gas. Wood Mackenzie further estimates total YTF potential in Vietnam to be at 2.43 billion boe of liquids and gas. A large portion of Vietnam’s gas reserves has remained undeveloped on account of historically low gas prices and a lack of adequate infrastructure.

Myanmar

Myanmar is currently the poster boy for E&P activity in South East Asia, given its vastly unexplored terrain, growing domestic demand for energy, and proximity to neighbouring markets which include Thailand, China and India. Myanmar’s energy Ministry estimates the country holds 17.5 Tcf of gas reserves and 3.2 billion barrels of crude oil. Offshore, Myanmar is principally dominated by gas, although little exploration has taken place so far. Most of the shallow offshore is largely under-explored whilst none of the deep offshore areas have been explored yet. There is significant enthusiasm for Myanmar’s prospective returns given the high rate of success from relatively little exploration thus far. Although there are several challenges including lack of financing, poor technical equipment, and the availability of skilled manpower, the Government of Myanmar is determined to take steps to address these concerns and help kick start the industry.

China

China has been adding an estimated 1 million-1.2 million b/d of refining capacity over 2012-2013 and is looking to enhance its downstream segment by an average of 1 million b/d annually between 2014-2018. Chinese nationwide refinery operating rates have averaged 77% in 2012 and 79% in 2013. There is a likelihood of utilization rates drifting lower on account of increasing refining capacity. Notwithstanding, China is expected to keep enhancing capacity as a policy, in line with its aim to become energy self-sufficient. The country also has a restrictive export policy barring a few Sino-foreign joint venture projects. However, whilst refining capacity grows unabated, there has been a moderate fall in consumption.

India

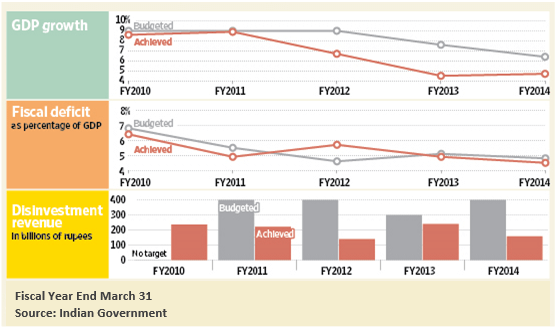

India has always been a leading energy consumer and as a result, the country constantly seeks to match an ever-increasing demand. During FY 2013–14, total consumption of petroleum products in India was 158.2 million tonnes (MT). The country had total reserves of 1354.76 billion cubic metres (BCM) of natural gas and 758.27 million metric tonnes (MMT) of crude oil at the end of FY 2012–13. By 2015–16, India’s demand for gas is expected to touch 124 MTPA, as per projections of India’s Petroleum and Natural Gas Ministry.

Indian NOCs (National Oil Corporations) have embarked on massive investment in the sector. Indian Oil Corporation Ltd (IOCL) through its wholly owned affiliate IndOil Montney Ltd, Canada, signed transaction agreements with Progress Energy Canada Ltd and PETRONAS Carigali Canada BV to acquire a 10 per cent stake in Progress Energy Canada’s LNG natural gas reserves in northeast British Columbia, as well as the proposed Pacific NorthWest LNG Ltd (PNW LNG) export facility located on Canada’s West Coast.

In other major recent industry developments:

- GAIL Ltd has entered into an agreement with Japan-based Chubu Electric Power Co to seek collaboration in the area of joint LNG procurement.

- Reliance Industries Ltd (RIL) has been awarded two offshore blocks, M17 and 18, in Myanmar’s offshore block bidding round of 2013.

- Prize Petroleum Company Ltd, a WOS subsidiary and upstream arm of Hindustan Petroleum Corporation Ltd (HPCL), has entered into a sale purchase agreement with M/s AWE, Australia to acquire 11.25 per cent stake in T/L1 license and 9.75 per cent stake in T/18P permit for a total consideration of US$ 79.66 million.

The Indian government has also taken prudent steps, by way of its’ Cabinet Committee on Investments (CCI), by clearing projects worth US$ 1.32 billion in the sector in December 2013. These projects involve companies such as Chennai Petroleum Corporation Ltd (CPCL), IOCL and HPCL. On the back of these measures India’s overall expenditure is expected to increase with its Pipeline and Fixed Platform markets likely to be the driving force behind these high capital expenditures.

Asian Outlook

Asia will continue to play a significant role internationally in the oil and gas industry. Given the expected increase in energy demand from developing countries, the region should see increased levels of offshore oil and gas activity.

Asia is characterized by large areas of shallow water, relative to other regions of the world, where fixed platforms are preferred. This is particularly the case with Malaysia and China where the fixed platform market will see the highest levels of growth in the region, according to experts. The entire region of Southeast Asia is expected to lead fixed platform expenditure. India and Malaysia are expected to lead investments for offshore pipelines.

Rising crude import reliance will encourage upstream acquisitions. Credit ratings agency Moody’s expects Asia’s growing reliance on crude oil and natural gas imports to fuel more international upstream acquisitions by National oil companies (NOCs) to secure long-term energy needs. Most Asian NOCs have comfortable headroom within their ratings for acquisitions, despite sizeable overseas investments over the past year. NOCs will continue to be the main focus of investment in the region, with IOC’s trailing close behind.